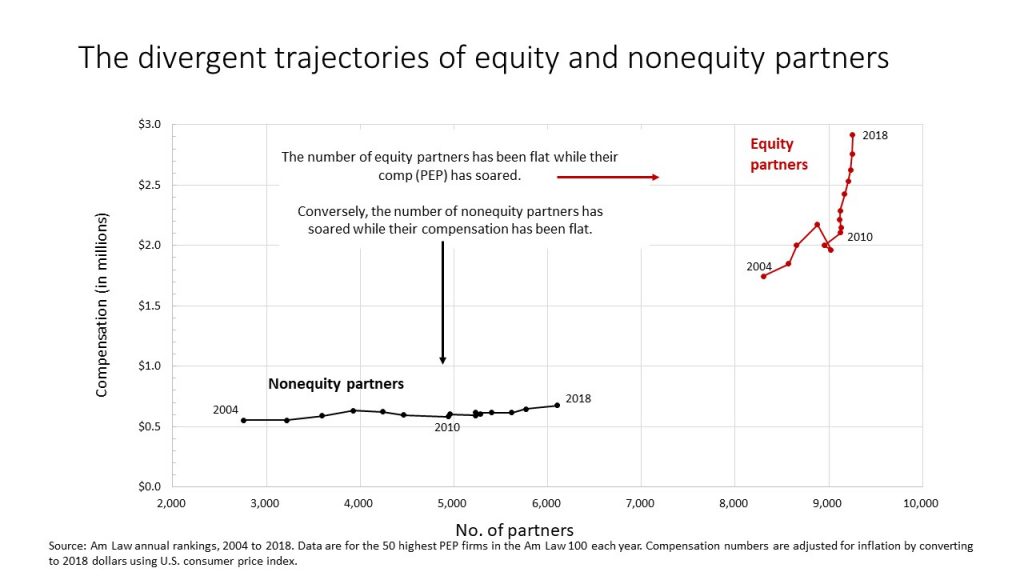

While the Am Law 100 reports are still being racked and stacked, one dynamic is already clear: 2018 witnessed little movement in the number of equity partners while their compensation (profits per equity partner) grew strongly; conversely, nonequity partner numbers grew strongly while their compensation was flat. This continues a trend going back over a decade that has been especially pronounced since 2010. To be clear, this is not an artifact of middle and lower tier firms—the data shown are for the 50 most-profitable firms in this year’s Am Law 100.

Law firm traditionalists will decry this dynamic as an erosion of the implicit social contract between firms and their senior lawyers and would-be equity partners. I see it differently: It’s evidence of law firm leaders coming to grips with market reality and managing through the constraints of outmoded traditions.