Outwit, Outplay, Outlast: A Post-Recession View of the Survivors

A decade later, we revisit the 2008 Am Law 200 for a look at how the Big Law game has changed. Spoiler alert: it's gotten much tougher to be a managing partner.

June 20, 2018 at 07:09 PM

15 minute read

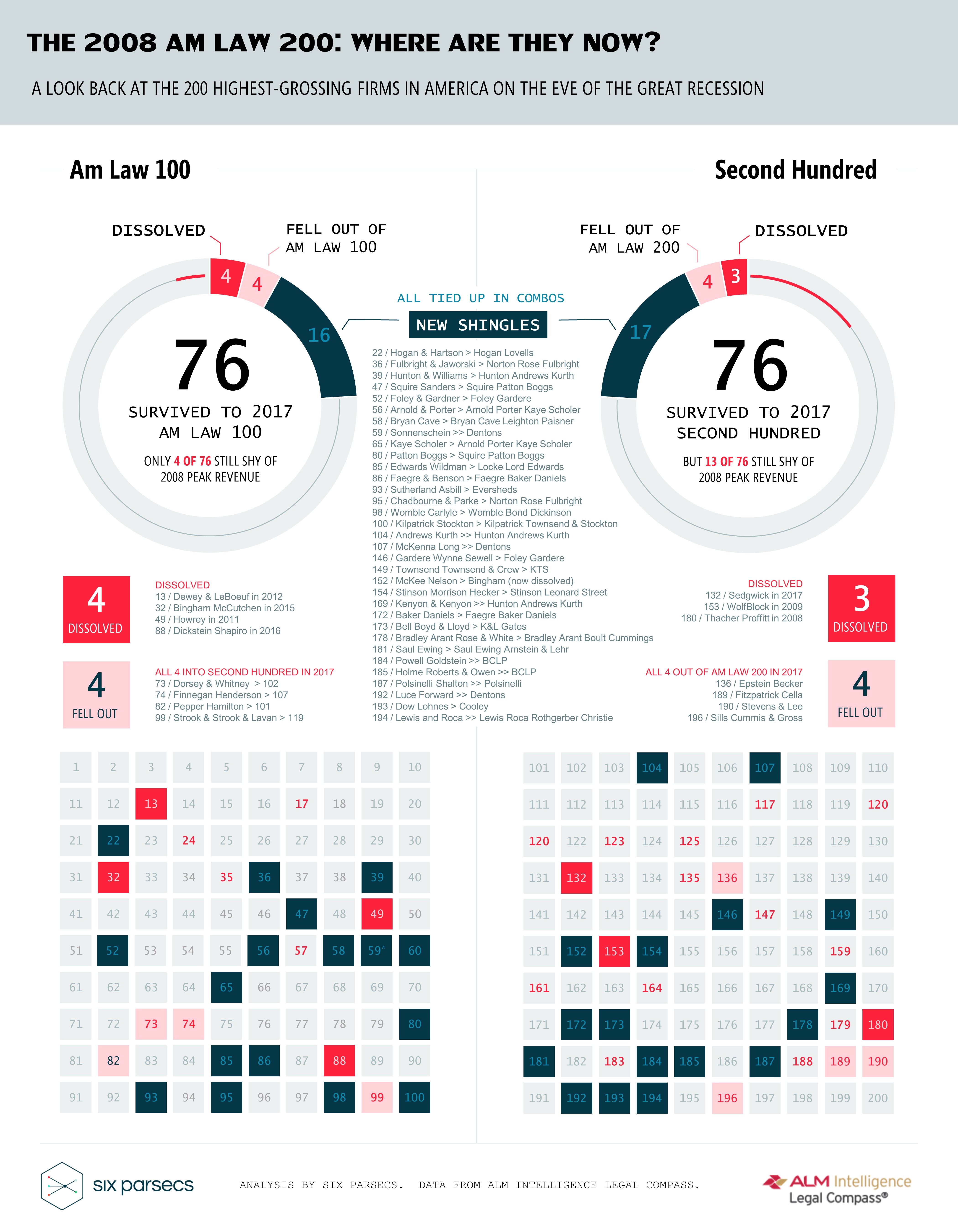

The modern American law firm is a beleaguered enterprise, beset on all sides by intensifying competitive pressures both new and old. By all accounts, law firm leaders know this to be a self-evident truth. You see it in your financials, you sense it in the air, and you feel it in your bones. And yet in 69 percent of law firms, partners resist most change efforts . Why the Disconnect? With all respect, we propose skipping the usual detour about the unique challenges of leading change among lawyers. Instead, we posit a more novel theory: survivorship bias. Survivorship bias is the logical error of focusing exclusively on the people that made it past a selection event—and ignoring those who did not. It occurs, at least in part, because the latter group no longer have visibility or voice. And we all fall prey to the availability heuristic : we base our judgments on what comes to mind most easily . It is the combination of survivorships bias and the availability heuristic that shapes the worldview of the working equity partner, creating an effective reality distortion field and presenting seemingly insurmountable communication challenges for most law firm leaders. Partners and Firm Leaders Experience the New Normal (Very) Differently In 2018, Big Law partners look around and see much the same world as they did in 2008. There are still 200 firms in the Am Law 200. The majority of those 200 firms hang on their doors old and prestigious names that are older and more prestigious than ever. In short, they only see the ones who have survived. For the working (read: revenue-generating) equity (read: voting) partner, most of the material changes in the New Normal have remained largely abstract. By and large, Big Law equity partners work and live in 2018 mostly as they did a decade ago: they practice law, they record their time, they try to bill and collect when asked, and they feel their compensation should be higher than it is. Meanwhile, most of the industry-wide response in Big Law after 2008 has placed emphasis on operational discipline, expense control, financial hygiene—and inorganic growth. Executive committees and administrative leaders have strained to cut costs, manage rates and AFAs, field an ever-growing brace of RFP-writing marketers, implement energetic lateral recruitment programs, and vet a constant parade of dance partners for a potentially game-changing combination. It fell to managing partners across Big Law to make difficult and unpopular decisions: to lay off associates and staff, to “manage out” underperforming partners, to spin up de-equitization programs that would help the profit pie split more palatably among the surviving equity partners. You and your peers across the industry have faced down these bruising battles and endured grueling workloads, all to outwit, outplay and outlast the competition, all for the collective good of “the firm.” But this is your day-to-day—neither observed nor experienced by any of your revenue-generating and voting constituency. Equity partners hear that the marketplace is changing ( because you, the managing partner, seem to talk of nothing else ) and yes, they see that some clients are very excited about a new set of buzzwords each year. In practice, most of these transformational changes translates into numberless policies that largely impinge on their time and autonomy: a new way to track billable hours, more rules to manage pricing and billing, a new process to submit expenses, a long list of reasons to adapt to a smaller office, constant pressure to embrace legal technology ( which keeps changing in mystifying ways and takes too much time to learn ), and the list goes on. All these developments have materialized in their lives in a way that is largely disembodied from a market crash that seems very far away now. They are all documented in internal memos ( too long, didn't read ) and delivered in internal meetings ( too busy, didn't attend ). To the working (read: revenue-generating) equity (read: voting) partner, all these distracting annoyances have one other thing in common. They all seem to have originated from or issued by you, the managing partner. Our Collective Memories Need (a Lot of) Help We all remember Dewey and Howrey. Both firms were high-profile and well-respected, their downfalls quick and surprising. The closures of Bingham McCutchen and Sedgwick are remembered because they are recent. But when all is said and done, most equity partners will struggle to name a dozen other law firm failures, and so we tend to think of law firm failures as rare. To be fair, in the grand scheme of things, dissolution is quite uncommon—but in 2018, the curtain call for a prestigious law firm can take many forms. Who remembers McKee Nelson, described by The American Lawyer as “one-of the pre-eminent firms for tax planning and tax litigation”? At its peak in 2006, McKee was a 120-strong firm that eventually whittled down to 30 lawyers by mid-2009 when it was absorbed rather unceremoniously by Bingham McCutchen. If any canonical annals of the history of Big Law existed, they would be peppered with stories of firms much like McKee. In lieu of such a comprehensive document, we revisited the 200 largest firms in America by 2008 revenues to see how they have fared a decade later. To establish a point of comparison, we also analyzed the 1998 class of the Am Law 200 and tracked their progress over the following decade.

The modern American law firm is a beleaguered enterprise, beset on all sides by intensifying competitive pressures both new and old. By all accounts, law firm leaders know this to be a self-evident truth. You see it in your financials, you sense it in the air, and you feel it in your bones. And yet in 69 percent of law firms, partners resist most change efforts . Why the Disconnect? With all respect, we propose skipping the usual detour about the unique challenges of leading change among lawyers. Instead, we posit a more novel theory: survivorship bias. Survivorship bias is the logical error of focusing exclusively on the people that made it past a selection event—and ignoring those who did not. It occurs, at least in part, because the latter group no longer have visibility or voice. And we all fall prey to the availability heuristic : we base our judgments on what comes to mind most easily . It is the combination of survivorships bias and the availability heuristic that shapes the worldview of the working equity partner, creating an effective reality distortion field and presenting seemingly insurmountable communication challenges for most law firm leaders. Partners and Firm Leaders Experience the New Normal (Very) Differently In 2018, Big Law partners look around and see much the same world as they did in 2008. There are still 200 firms in the Am Law 200. The majority of those 200 firms hang on their doors old and prestigious names that are older and more prestigious than ever. In short, they only see the ones who have survived. For the working (read: revenue-generating) equity (read: voting) partner, most of the material changes in the New Normal have remained largely abstract. By and large, Big Law equity partners work and live in 2018 mostly as they did a decade ago: they practice law, they record their time, they try to bill and collect when asked, and they feel their compensation should be higher than it is. Meanwhile, most of the industry-wide response in Big Law after 2008 has placed emphasis on operational discipline, expense control, financial hygiene—and inorganic growth. Executive committees and administrative leaders have strained to cut costs, manage rates and AFAs, field an ever-growing brace of RFP-writing marketers, implement energetic lateral recruitment programs, and vet a constant parade of dance partners for a potentially game-changing combination. It fell to managing partners across Big Law to make difficult and unpopular decisions: to lay off associates and staff, to “manage out” underperforming partners, to spin up de-equitization programs that would help the profit pie split more palatably among the surviving equity partners. You and your peers across the industry have faced down these bruising battles and endured grueling workloads, all to outwit, outplay and outlast the competition, all for the collective good of “the firm.” But this is your day-to-day—neither observed nor experienced by any of your revenue-generating and voting constituency. Equity partners hear that the marketplace is changing ( because you, the managing partner, seem to talk of nothing else ) and yes, they see that some clients are very excited about a new set of buzzwords each year. In practice, most of these transformational changes translates into numberless policies that largely impinge on their time and autonomy: a new way to track billable hours, more rules to manage pricing and billing, a new process to submit expenses, a long list of reasons to adapt to a smaller office, constant pressure to embrace legal technology ( which keeps changing in mystifying ways and takes too much time to learn ), and the list goes on. All these developments have materialized in their lives in a way that is largely disembodied from a market crash that seems very far away now. They are all documented in internal memos ( too long, didn't read ) and delivered in internal meetings ( too busy, didn't attend ). To the working (read: revenue-generating) equity (read: voting) partner, all these distracting annoyances have one other thing in common. They all seem to have originated from or issued by you, the managing partner. Our Collective Memories Need (a Lot of) Help We all remember Dewey and Howrey. Both firms were high-profile and well-respected, their downfalls quick and surprising. The closures of Bingham McCutchen and Sedgwick are remembered because they are recent. But when all is said and done, most equity partners will struggle to name a dozen other law firm failures, and so we tend to think of law firm failures as rare. To be fair, in the grand scheme of things, dissolution is quite uncommon—but in 2018, the curtain call for a prestigious law firm can take many forms. Who remembers McKee Nelson, described by The American Lawyer as “one-of the pre-eminent firms for tax planning and tax litigation”? At its peak in 2006, McKee was a 120-strong firm that eventually whittled down to 30 lawyers by mid-2009 when it was absorbed rather unceremoniously by Bingham McCutchen. If any canonical annals of the history of Big Law existed, they would be peppered with stories of firms much like McKee. In lieu of such a comprehensive document, we revisited the 200 largest firms in America by 2008 revenues to see how they have fared a decade later. To establish a point of comparison, we also analyzed the 1998 class of the Am Law 200 and tracked their progress over the following decade.  Our analysis surfaced the following 4 trends:

Our analysis surfaced the following 4 trends:

- Large law firms are relatively resilient. Relative to corporate America, a 76 percent survival rate over a decade is still fairly cushy. For context, the 20-year survival rate for the Fortune 500 is an unforgiving 38 percent, while roughly 60 percent of the 1998 class of the Am Law 200 made it into the 2017 rankings with their shingles intact. This is, however, cold comfort for many of the firms that haven't yet managed to recapture the prosperity of the pre-recession years.

- The stakes got much higher post-recession. Of the 1998 Am Law 200, nine firms disbanded over the following decade while 24 firms had merged into new shingles by 2007. While those numbers don't seem too different from the track record of the 2008 class, the difference lies in the size and scale of firms involved.

Prior to 2008, Brobeck was a headline-dominating law firm failure; at its peak in 2002, the firm reported attorney headcount of 792 and revenue of $353 million. In comparison, Dewey's peak in 2008 and eventual fall were much grander in scale: at one time, it claimed membership to an elite group of firms with over $1 billion in revenue, but it reported more than $300 million in debt by the time it shuttered in the largest law firm bankruptcy in history. At its peak, Bingham McCutchen posted $873 million in revenues, generated by 900 lawyers in 14 offices globally.

- A few megafirms emerged from daisy-chained mergers and serial acquirers. Like firm failures, mergers got grander in scale after 2008—but this happened more gradually in tandem with the progression of combinations.

The rise of DLA Piper into a perennial top 5 firm by revenue and truly global powerhouse began nearly 20 years ago in a series of regional consolidations: the 1999 merger of Baltimore-based Piper & Marbury and Chicago-based Rudnick & Wolfe (at the time, the largest firm merger in history), the 2002 acquisition of D.C.-based Verner Liipfert, a 3-way merger in 2004 with San Diego-based Gray Cary and the UK-based DLA LLP, culminating in a tie-up with DLA Phillips Fox in 2011. Similarly, K&L Gates was formed over a series of tie-ups from 2005 to 2009 that combined U.S. regional firms in the Atlantic Mideast, Pacific Northwest, Texas, Southeast, Midwest, and topped off by a cross-border combination in 2013 with Australian firm Middletons.

- Combined firms are invading the upper reaches. Norton Rose Fulbright made its debut into the Am Law rankings in 2013 by posting $1.9 billion in gross revenues—one of only 24 firms in the 3-comma-club that year. The combinations of Squire Sanders with Patton Boggs as well as Arnold & Porter with Kaye Scholer vaulted the newly shingled firms into the Am Law 50; the same will be true of Bryan Cave Leighton Paisner and Hunton Andrews Kurth next year.

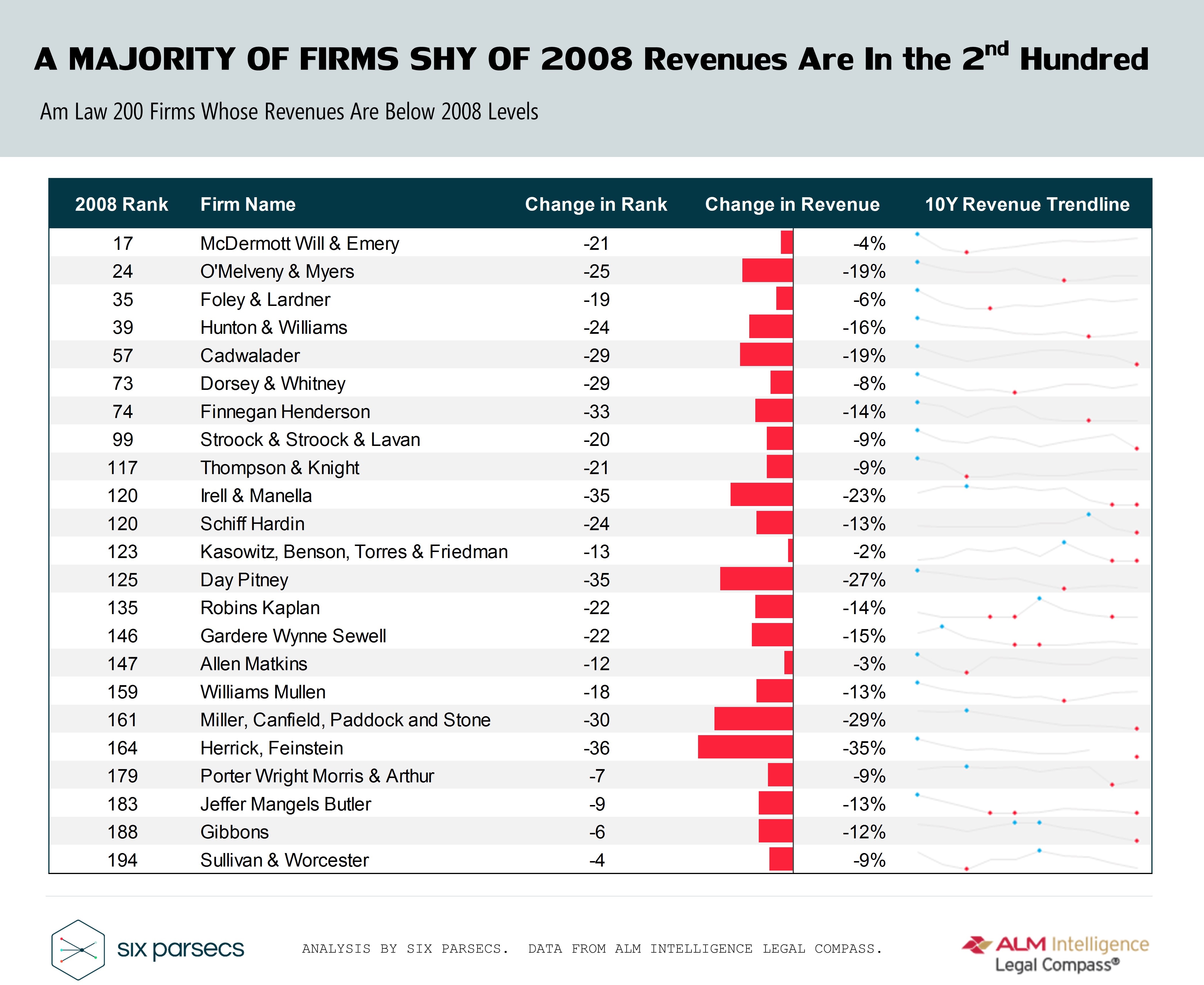

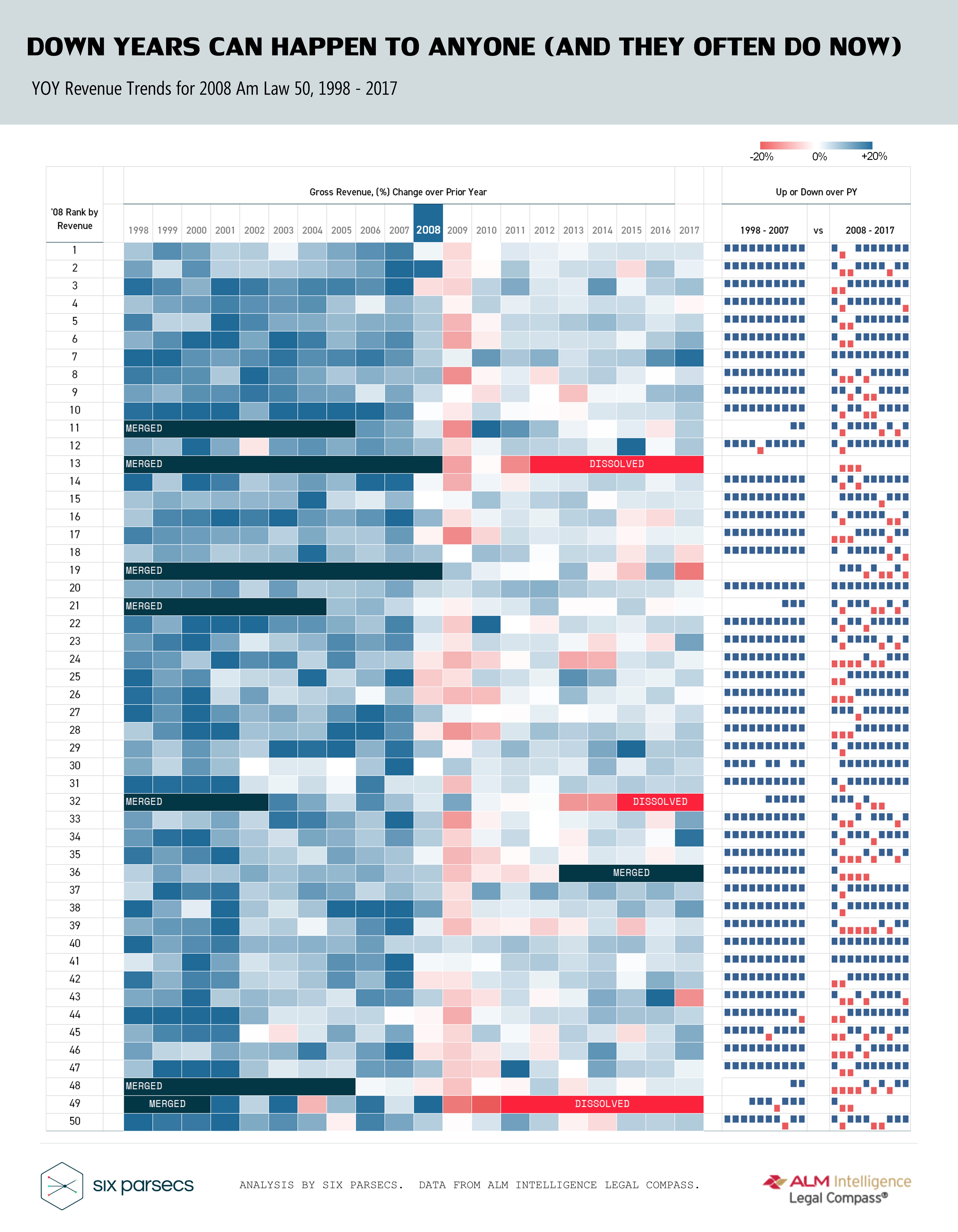

The Siren Song of Growth Whispers “Bigger IS Better” These trends conspire to create a much more complicated and much less hospitable competitive landscape for firms. The most meaningful implication of the post-recession landscape relates to the perennial focus on law firm growth. In 2008, the top grossing firm was Skadden with $890 million in revenue; in 2017, Kirkland overtook the top spot with $3.2 billion, displacing Latham, which also posted revenues in excess of the $3 billion. Ten years ago, only Baker McKenzie, Jones Day, Latham, and White & Case reported head count exceeding 2,000 lawyers for 9 percent share of total Am Law 200 head count. In 2017, seven firms reported headcount of 2,000 or more, accounting for 17 percent of all lawyers in the Am Law 200. As the bulk of the Am Law 200 shifts toward larger headcount and higher revenues, a baseline level of growth has been necessary for firms looking to keep up with the Joneses. Both Kasowitz Benson Torres and Allen Matkins are just shy of their 2008 revenue levels, yet both firms have tumbled about a dozen spots in revenue rankings. Pepper Hamilton has moved down 19 spots since 2008 despite posting 2017 revenues that outperformed its pre-recession peak by about $10 million. Over the last decade, the size and shape of the Am Law 200 has evolved very differently at the extreme ends. The smallest firms in the 2017 Am Law 200 are smaller than the smallest firms in the 2008 class by both size and revenue. As seen below, a clear majority of the firms still shy of their 2008 revenues are in Second Hundred firms.  Aggregate market-level analyses often show the Am Law 100 outperforming the Second Hundred. From 2008 to 2017, the U.S. Census estimates 18 percent growth in revenue for legal services sector. From the 2008 Am Law 100, 61 firms managed to outpace the industry in revenue growth, while only 51 of the 2008 Second Hundred firms managed the same feat. Taken out of context, these statistics fuel the mistaken notion that size can provide sufficient competitive advantage—a common but dangerous strategy trap. The New Normal, in One Picture To say that demand is flat is intrinsically abstract. Most equity partners understand the academic concept of supply and demand, and it is galactically obvious to all concerned parties that flat demand is worse than growing demand. What is less obvious is how flat demand practically affects the business of the modern law firm. For managing partners struggling to communicate the extent of structural changes in the legal marketplace—or the challenges they imply for Am Law 200 firms wishing to remain so hereafter—we provide a visual aid.

Aggregate market-level analyses often show the Am Law 100 outperforming the Second Hundred. From 2008 to 2017, the U.S. Census estimates 18 percent growth in revenue for legal services sector. From the 2008 Am Law 100, 61 firms managed to outpace the industry in revenue growth, while only 51 of the 2008 Second Hundred firms managed the same feat. Taken out of context, these statistics fuel the mistaken notion that size can provide sufficient competitive advantage—a common but dangerous strategy trap. The New Normal, in One Picture To say that demand is flat is intrinsically abstract. Most equity partners understand the academic concept of supply and demand, and it is galactically obvious to all concerned parties that flat demand is worse than growing demand. What is less obvious is how flat demand practically affects the business of the modern law firm. For managing partners struggling to communicate the extent of structural changes in the legal marketplace—or the challenges they imply for Am Law 200 firms wishing to remain so hereafter—we provide a visual aid.  The above highlight table shows the YOY revenue changes for the 2008 Am Law 50. Firm names and actual percentage figures have been omitted to emphasize the drastic, structural change wrought by the Great Recession. In particular, the final pair of columns on the right paint a fairly clear picture of how much tougher the Big Law game has become in the last decade. In the decade prior to the subprime meltdown, Am Law firms did not have down years, particularly in the upper echelons. It just did not happen because the industry-wide demand growth was that good . This is no longer the reality we occupy. Am Law 200 firms now compete in an environment of ever-present demand volatility and unprecedented margin pressure. Down years can happen to any firm—regardless of size. In a largely flat market, most law firms are finding that it is now stunningly, unbelievably difficult to acquire new revenue organically. This is at least in part why firms remain so dependent on inorganic growth. The bargaining power of clients is already quite high due to the perennial cost pressures placed on corporate law departments. While the insourcing trend may be nearing its natural peak, client pressure to step up solution-orientation, client service, and pricing sophistication are likely to further intensify in tandem with the continuing maturation of the legal operations function . Meanwhile, bargaining power of talent is on the rise . Associate compensation is on the agenda yet again, and the perennially frothy lateral market chips away slowly but surely at the stability of the partnership structure. Other existential threats, albeit more remote, loom on the horizon as the Big 4 , ALSPs and legal tech companies probe for an opening to shave away precious market share from incumbent law firms. Playing for size won't be enough to defend against these threats. The firms hoping to survive—or perhaps even thrive—to see their shingles make it intact into the 2027 Am Law 200 must compete more intensely, think more creatively, and act more decisively than ever before. Notes on Data Reliability Since data reliability is an ever-present issue in legal market analysis, we append a few notes. The tie-ups noted here are limited to new shingles. This leaves out of the analysis those survivors who relied upon less visible means of inorganic growth, including aggressive recruitment of lateral talent, and acquisitions of operations too small to make the Am Law 200 cut. A review of merger data over a similar period suggests that the snapshot of the Am Law 200 is far more likely to understate (rather than overstate) the overall level of reliance on inorganic growth. From 2007 to 2016, Altman Weil Mergerline reported 688 law firm combinations, with 89 percent of them classified as acquisitions rather than “true mergers,” defined as a combination in which the larger firm is no more than twice the size of the smaller. Of all acquisitions, 78 percent of combinations involved lateral groups of 2 to 20 lawyers. Most of these deals occur outside of the Am Law 200. While those omissions mean that this snapshot does not represent a comprehensive representation of the entire legal services market, the discernible trends here are still significant and meaningful for the segment covered in the analysis. Jae Um is founder and executive director of Six Parsecs. She is an ALM Intelligence Fellow.

The above highlight table shows the YOY revenue changes for the 2008 Am Law 50. Firm names and actual percentage figures have been omitted to emphasize the drastic, structural change wrought by the Great Recession. In particular, the final pair of columns on the right paint a fairly clear picture of how much tougher the Big Law game has become in the last decade. In the decade prior to the subprime meltdown, Am Law firms did not have down years, particularly in the upper echelons. It just did not happen because the industry-wide demand growth was that good . This is no longer the reality we occupy. Am Law 200 firms now compete in an environment of ever-present demand volatility and unprecedented margin pressure. Down years can happen to any firm—regardless of size. In a largely flat market, most law firms are finding that it is now stunningly, unbelievably difficult to acquire new revenue organically. This is at least in part why firms remain so dependent on inorganic growth. The bargaining power of clients is already quite high due to the perennial cost pressures placed on corporate law departments. While the insourcing trend may be nearing its natural peak, client pressure to step up solution-orientation, client service, and pricing sophistication are likely to further intensify in tandem with the continuing maturation of the legal operations function . Meanwhile, bargaining power of talent is on the rise . Associate compensation is on the agenda yet again, and the perennially frothy lateral market chips away slowly but surely at the stability of the partnership structure. Other existential threats, albeit more remote, loom on the horizon as the Big 4 , ALSPs and legal tech companies probe for an opening to shave away precious market share from incumbent law firms. Playing for size won't be enough to defend against these threats. The firms hoping to survive—or perhaps even thrive—to see their shingles make it intact into the 2027 Am Law 200 must compete more intensely, think more creatively, and act more decisively than ever before. Notes on Data Reliability Since data reliability is an ever-present issue in legal market analysis, we append a few notes. The tie-ups noted here are limited to new shingles. This leaves out of the analysis those survivors who relied upon less visible means of inorganic growth, including aggressive recruitment of lateral talent, and acquisitions of operations too small to make the Am Law 200 cut. A review of merger data over a similar period suggests that the snapshot of the Am Law 200 is far more likely to understate (rather than overstate) the overall level of reliance on inorganic growth. From 2007 to 2016, Altman Weil Mergerline reported 688 law firm combinations, with 89 percent of them classified as acquisitions rather than “true mergers,” defined as a combination in which the larger firm is no more than twice the size of the smaller. Of all acquisitions, 78 percent of combinations involved lateral groups of 2 to 20 lawyers. Most of these deals occur outside of the Am Law 200. While those omissions mean that this snapshot does not represent a comprehensive representation of the entire legal services market, the discernible trends here are still significant and meaningful for the segment covered in the analysis. Jae Um is founder and executive director of Six Parsecs. She is an ALM Intelligence Fellow. ![]()

NOT FOR REPRINT

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Trending Stories

- 1The Law Firm Disrupted: For Big Law Names, Shorter is Sweeter

- 2Wine, Dine and Grind (Through the Weekend): Summer Associates Thirst For Experience in 'Real Matters'

- 3The 'Biden Effect' on Senior Attorneys: Should I Stay or Should I Go?

- 4BD Settles Thousands of Bard Hernia Mesh Lawsuits

- 5First Lawsuit Filed Alleging Contraceptive Depo-Provera Caused Brain Tumor

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250