![]() It is heard so often it has the aura of incontrovertible truth: the legal market is stratifying; the Am Law 50 firms are pulling away from the Am Law second fifty, the Am Law second fifty is pulling away from the Am Law second hundred, etc. The strategy implications are profound: position is destiny—if you’re a smaller firm, you need to bulk up to avoid falling further and further behind. It’s sound strategic reasoning. The problem? The underlying premise is entirely false: the market is not stratifying. What jumps out from the data is that performance is stunningly variable across firms of all sizes and profitability levels. Put differently: position is not destiny; any firm can grow revenues and profitability strongly.

It is heard so often it has the aura of incontrovertible truth: the legal market is stratifying; the Am Law 50 firms are pulling away from the Am Law second fifty, the Am Law second fifty is pulling away from the Am Law second hundred, etc. The strategy implications are profound: position is destiny—if you’re a smaller firm, you need to bulk up to avoid falling further and further behind. It’s sound strategic reasoning. The problem? The underlying premise is entirely false: the market is not stratifying. What jumps out from the data is that performance is stunningly variable across firms of all sizes and profitability levels. Put differently: position is not destiny; any firm can grow revenues and profitability strongly.

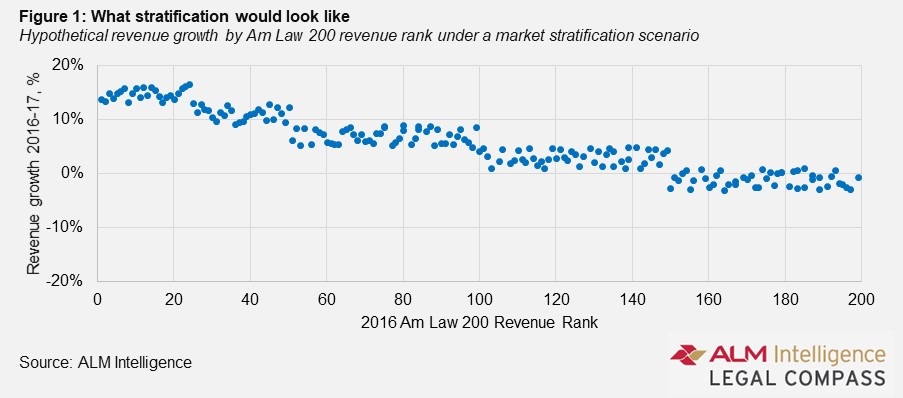

Let’s start with what stratification would look like. If we lined up the Am Law 200 firms from largest to smallest (horizontal axis) and plotted the revenue growth of each firm (vertical axis) we’d see something like Figure 1: clusters of similar growth rate for firms in the various size ‘strata’ with steps down in growth rate as we move from strata of larger to smaller firms (left to right).