Below is an excerpt of Barbarians at the Gate: The Invasion of Regional Legal Markets and How Mid-sized Firms Should Respond. The full report is available on the ALM Intelligence website.

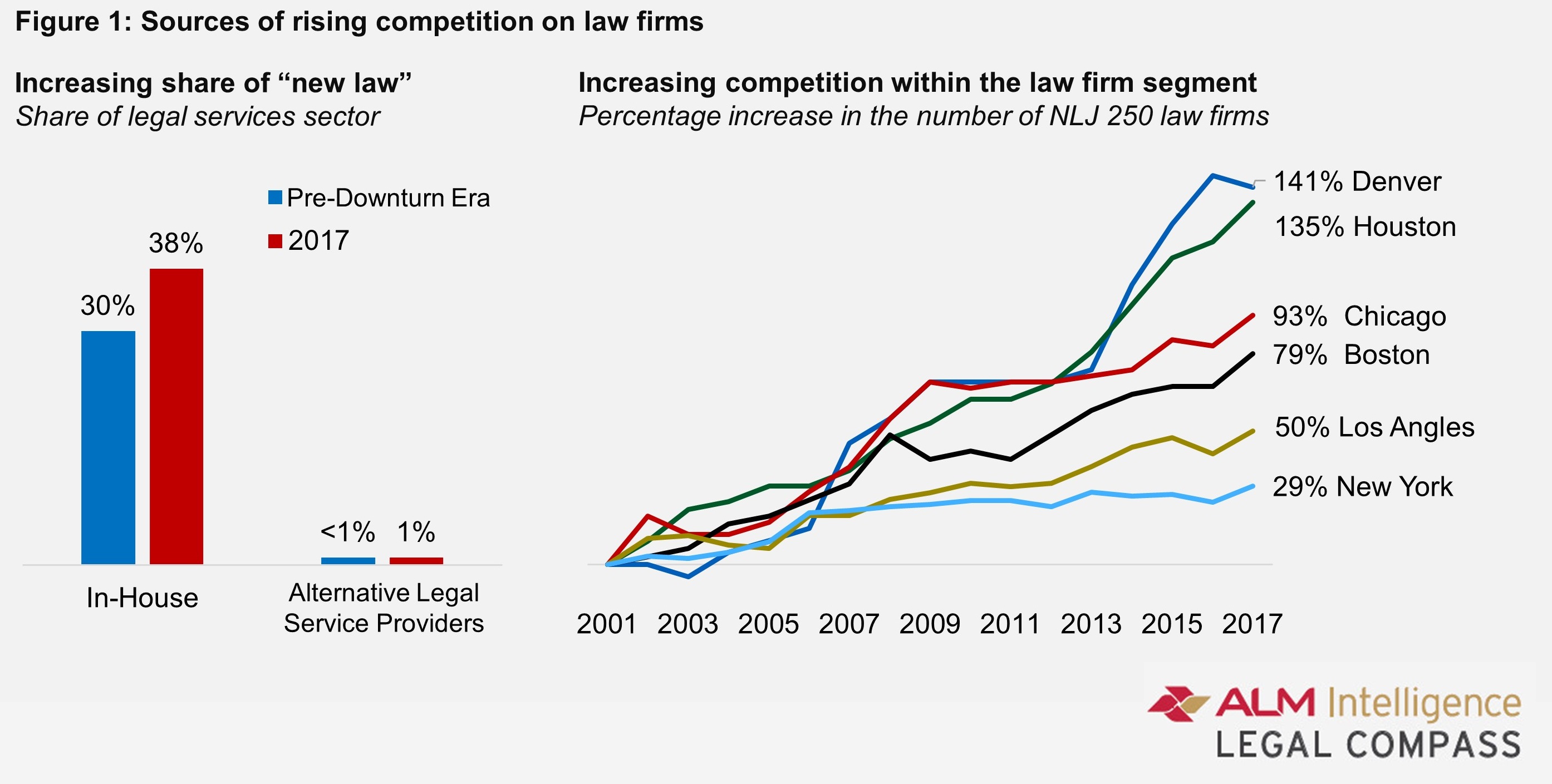

Rising competition has been a major discussion in the legal industry over the past decade. Most of that conversation, at least recently, has been focused on the competition flowing from new competitors such as alternative service providers and from the increased insourcing of in-house legal teams. The data on law firms’ geographic expansion over the past two decades suggests there is a third important source driving increased competition on law firms – notably other law firms (see Figure 1).