It’s conventional wisdom that the way for a firm to build its stature is to broaden its set of practice offerings. I hear partners say things like “All the top firms have a New York corporate practice; we should have one too” or “Great firms like Latham have tons of practices; we need to be like those guys”.

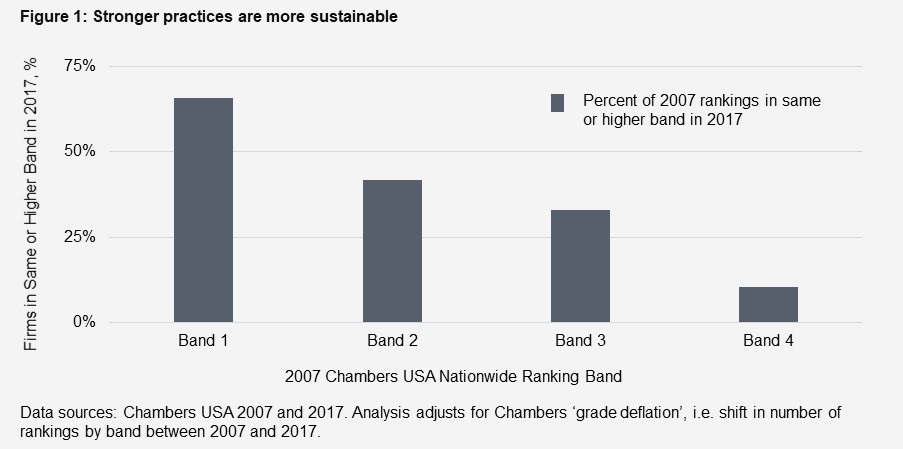

This is nuts. Or, to be polite, this is counter to what the data show. Take a look at Figure 1. It examines 2007 Chambers rankings and shows, for each ranking band, the percent of firm rankings that were in the same or higher band a decade later, i.e. the percent that sustained or improved their band ranking from 2007 to 2017, (details of the calculation in “About the analysis” below). The data show that stronger practices are more sustainable: the higher the band, the greater the probability of a firm’s ranking holding or improving. For example: while two-thirds of Band 1 rankings were held, barely one-in-ten Band 4 rankings were held or rose, (i.e. 90 percent of practices in Band 4 had descended to Band 5, or were no longer ranked, a decade later). Although the analysis here looks at practice strength for those achieving Chambers USA Nationwide status, the same dynamics likely hold in other domains: the stronger the practice, the more likely it is to sustain or gain in strength.