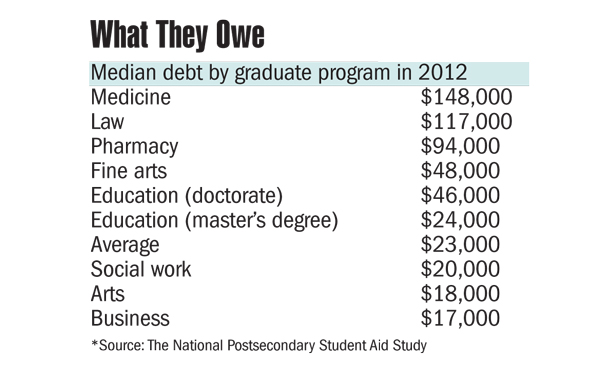

Law schools don’t prepare graduates for the financial realities they’ll face when their student loans come due, an American Bar Association task force has concluded after a year spent examining legal education costs. Next week, the House of Delegates will take up a proposal to fix that.

The resolution calls upon law schools to offer students better financial counseling and to disclose more information about financial aid and their own revenues. It also urges schools and loan providers to give borrowers easy-to-understand terms, and asks schools to experiment with ways to lower tuition.