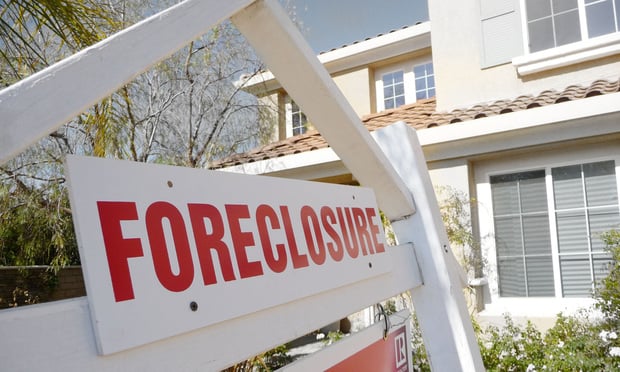

As the nation’s banking system teetered toward collapse in the fall of 2008, the federal government authorized a program to help homeowners facing foreclosure lower their mortgage payments. New York State followed suit with legislation requiring lenders to negotiate in “good faith” at court supervised settlement conferences before they could move forward with foreclosures.

Five years later, there is mounting evidence that lenders have hobbled New York’s effort through intransigence and incompetence. Since Jan. 1, 2013, 21 New York trial judges in nine counties have issued at least 24 rulings citing banks for failure to negotiate in good faith.1